This guide explains what vendor notes are and explains how vendor financing works. It goes into detail about how these arrangements are structured and why they are beneficial. Here are some key takeaways about vendor financing and vendor notes:

Vendor financing is when a vendor lends a business money in order to purchase their products.

Vendor notes are a form a subordinated debt that results from the vendor financing arrangement. Vendor notes go on a company’s balance sheet as a liability.

Vendor financing is often used by businesses trying to expand that can’t afford to pay for the inventory required out of cash.

Often vendor financing is used to finance expansion when the business can’t get traditional term loans—as is often the case with smaller businesses.

Vendor notes are a type of subordinated debt, meaning that these lenders get paid back after the business has repaid all of its other loans in the event of a bankruptcy, default, or sale.

Special Offer For Entrepreneurs

Learn How We Empower Agile Entrepreneurs With The Same Financial Acumen And Strategic Insight As Fortune 500's

A vendor note is a short-term loan that a vendor makes to a customer (a business wanting to buy its products) so that the customer can buy the vendor’s products.

This is a common type of financing when a business needs to finance its expansion but doesn’t have the ability to pay for the inventory it needs out of cash. This vendor financing allows the lender to make a sale and support a customer through a growth transition and it allows to business the ability to finance growth without traditional term loans.

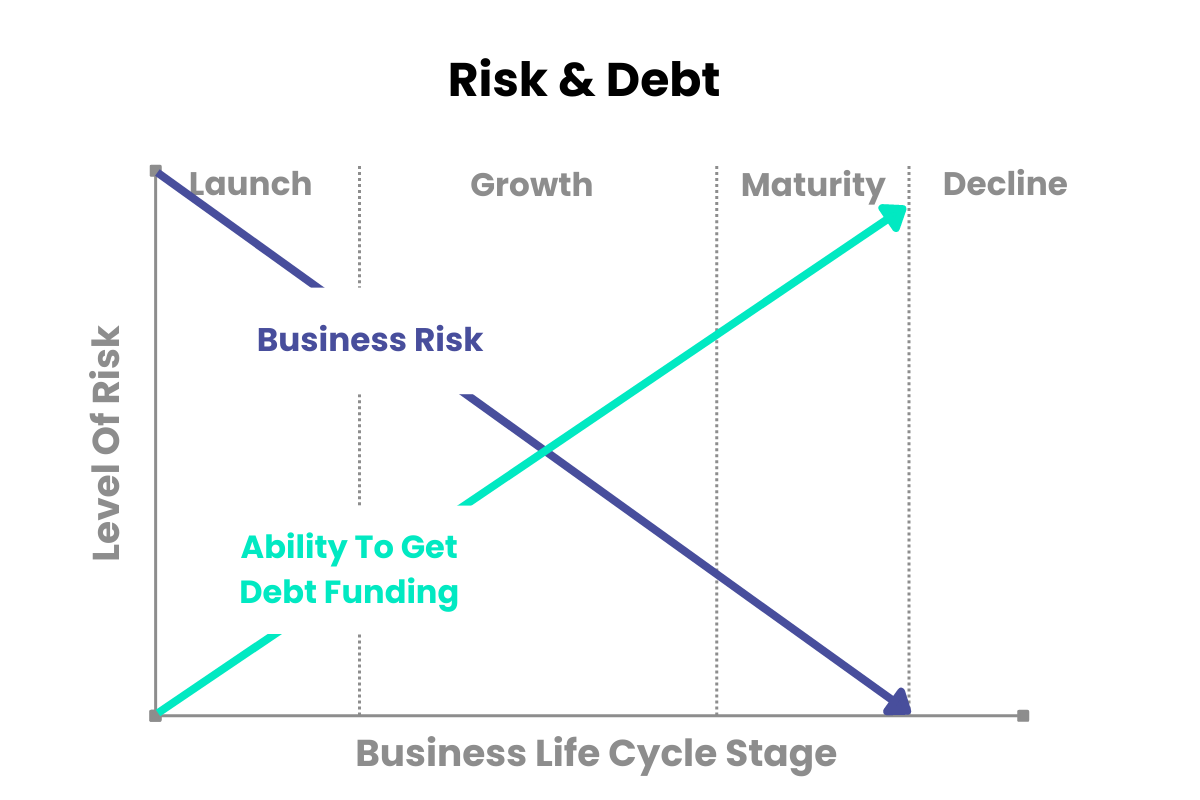

On this point, vendor notes are also more common in businesses that haven’t been around long enough to establish a proven track record yet. The infographic below illustrates the business lifecycle through the stages of launch, growth, maturity, and decline.

Commercial lenders like to see a historical track record of a business’ financial performance. They want to be able to assess the borrower’s ability to make payments on the debt they lend. This is why new businesses find it difficult if not impossible to use senior debt financing in their early stages. The infographic below illustrates the relationship between a lender’s perceived risk and a business’ ability to get debt funding—and how this changes over time as the business builds more of a financial track record.

Vendor financing gives businesses a financing option that is often based more on the working business relationship between the vendor (lender) and the customer (the business borrowing). The vendor understands that the business is growing and by financing their growth, they likely increase the volume of inventory their customer will buy in the future.

How Vendor Financing Works:

Vendor financing is typically structured in one of two ways. Remember that vendor financing refers to the arrangement of a business borrowing from a vendor, and a vendor note is the resulting subordinated debt from this arrangement.

The first is a debt arrangement where the business buys inventory from the vendor and agrees to pay interest on the loan. Generally, in these arrangements the interest accrues as time progresses. Meaning that the sooner the business repays the vendor note, the less interest it will pay.

The second way that vendor financing is commonly structured is when the vendor provides the business with the inventory it needs in exchange for stock (an equity stake) in the borrowing business. This is a less common arrangement as it comes at the expense of diluting equity. Often, it would be better to wait and finance slower growth organically than to give equity away in order to grow faster. However, the advantage to this arrangement is that the business borrowing doesn’t need to make interest payments, and therefore doesn’t have the extra drain on cashflow that it would with a traditional vendor financing debt arrangement. When these arrangements are agreed upon, they can act as a stepping stone to vertical integration. Vertical integration is where a business acquires or merges with another business along its supply chain.

Kimberly Advisors is a middle-market investment bank uniquely positioned to help business owners profit through M&A. In addition to M&A transaction brokering, we deliver detailed guidance on growing business value, comprehensive exit planning, and the confidence that comes from partnering with a seasoned M&A advisory team.

%20(1).png)

.png)