This guide explains what the capital stack is and the rationale behind making decisions about a business’ capital structure. Additionally, we’ll look at how a business’ capital stack is influenced by the lifecycle stage the business is currently in. Here are some quick takeaways about the capital stack:

The capital stack shows us how a company is financed, and it is a breakdown of a company’s capital structure.

The capital stack looks at how a business finances its operations through a mix of both debt and equity.

Debt and equity have different liquidity positions and these liquidity positions influence the expected return that investors are looking for from an investment.

Generally, the capital stack is broken down as senior debt, subordinated debt, and equity. (See the infographic above.)

Special Offer For Entrepreneurs

Learn How We Empower Agile Entrepreneurs With The Same Financial Acumen And Strategic Insight As Fortune 500's

The capital stack is generally broken down into three categories: senior debt, subordinated debt, and equity. It will be helpful to refer to the infographic to better understand this section.

The components of the capital stack are better understood through risk vs return. Senior debt has the lowest risk and the lowest return. Subordinated debt has more risk and a higher return than senior debt, but less than equity. Equity has the highest risk and generally offers the highest return on investment.

Senior debt is debt with the highest claim to a business’ cash flow. This means that these lenders get paid back before other lenders, making senior debt less risky than subordinated debt or equity investments. Senior debt also typically has the lowest interest rate, reflecting the risk vs reward scenario in lending to a business. Common types of senior debt include revolving lines of credit and term loans. To learn more about senior debt, read our guide: Senior Debt.

Subordinated debt has a higher liquidity position than equity, but subordinated debt is paid back after senior debt. Subordinated debt is used to fill the funding gap. Subordinated debt includes high-yield bonds, mezzanine debt, PIK notes, and vendor notes. Understanding subordinated debt is slightly more complicated than senior debt. The reason is that certain types of subordinated debt dilute equity. This happens when there are convertible options. When these options are exercised, they convert into equity—most commonly common shares. To learn more about subordinated debt, read this guide.

Equity is ownership in the business. Equity includes common stock, preferred stock, and shareholder loans. Equity has a lower liquidity position than senior and subordinated debt meaning equity investors get paid after debt investors.

Common shares represent the last liquidity position for investors. If a business is sold or liquidated common share owners are left with whatever remains after all debt has been repaid and all of the other types of equity are paid out. Common shares also have the last dividend paying position. So, whatever is left after a preferred dividend is paid is left for common dividends. Preferred shares have a higher liquidity position and dividend priority than common shares do. Last, we have shareholder loans, which are the highest equity liquidity position, but shareholder loans pay interest, not dividends. To learn more about equity financing read this guide.

Capital Stack: Debt vs Equity:

This section will expand on what we’ve learned about the capital stack so far and explain the rationale behind choosing debt or equity.

First, we’ll look at equity and try to understand why someone would want to give an ownership stake of their business in order to finance growth. Then we’ll look at debt and some pros and cons to raising capital with debt.

To understand why a business would want to raise capital with equity we need to understand the pros and cons to working with equity investors.

First, equity has no mandatory interest payments or fixed repayments. Second, depending on how term loans are structured, there may be maturity dates when the principle is to be repaid. With equity there are no maturity dates when a fixed lump sum must be repaid to the lender. This also contributes to creating more operational flexibility for the team running the business, as cash flow isn’t tied up in the repayment of loans or other debt.

A potential drawback to raising capital with equity is that investors become shareholders and therefore get an ownership stake and gain a degree of control through voting rights. Another drawback to raising money with equity is that the investors will generally expect a high return on their investment. Remember, equity has the lowest liquidity position, meaning that these investors get paid back after all debt has been repaid. Equity investors usually require a higher rate of return to offset the potential risk of investing in a lower liquidity position. Finally, equity comes at a higher cost of capital than debt does.

Now we’ll look at why a company would choose to raise capital through debt, as opposed to equity. Businesses use debt for two main reasons. The first is to avoid equity dilution, and the second is to lower the cost of capital. Debt has a lower cost of capital than equity does. Additionally, because debt investors have a higher claim to a business’s cash flow, they are in a safer position from a risk standpoint and will therefore usually require a lower rate of return than equity investors would.

Some drawbacks to debt are that it comes with interest payments and has a fixed repayment schedule, so it has more of a drain on the cashflow of a business. This can also create some operational rigidity, meaning that management has to work around the fixed repayment schedule and the effects that it has on cash flow. Debt investors get paid before equity investors and loans typically come with covenants meaning that financial performance standards must be met. Debt also comes with the inherent risk that if the business cannot repay the loans as agreed, the lender can call in the debt and the business may need to file for bankruptcy if it can’t meet its obligations.

Capital Stack & Business Lifecycle:

Now that we understand the capital stack and the rationale behind deciding to raise capital with debt vs equity, we’ll look at the practical reality of this decision.

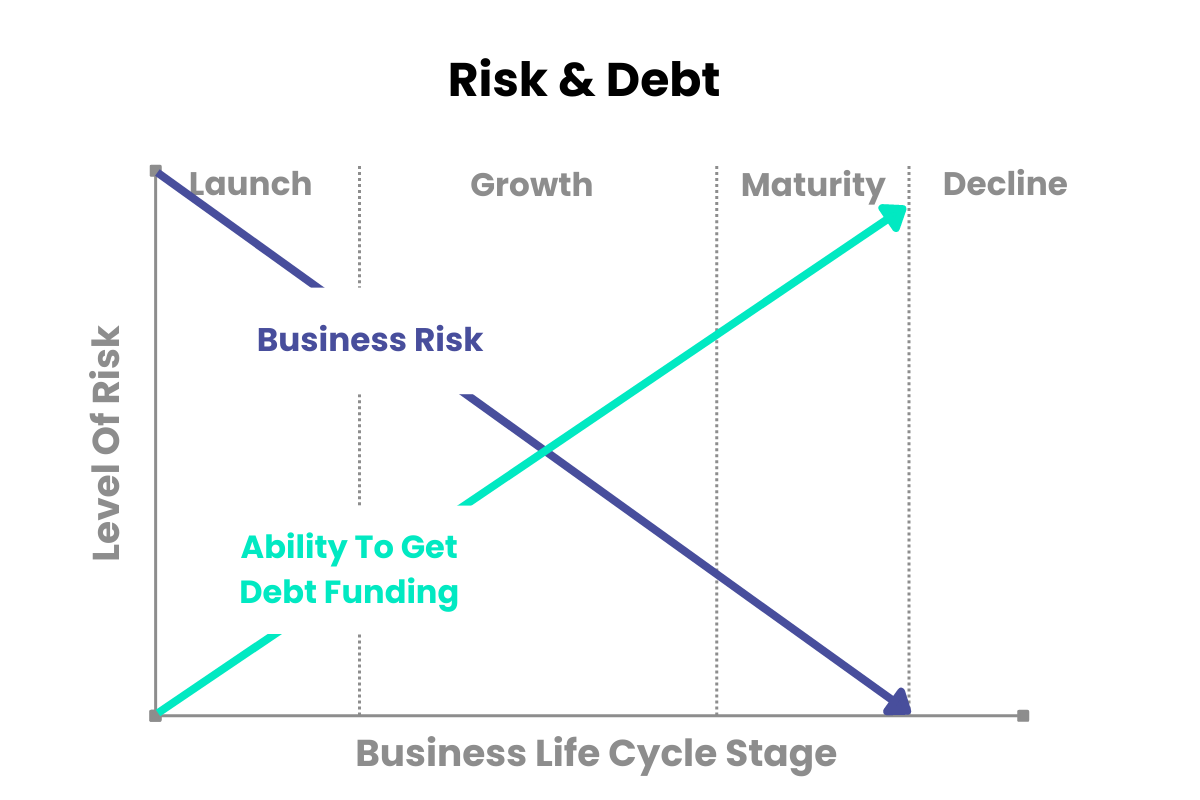

To understand this, we need to understand the business lifecycle. The infographic below shows the typical lifecycle of a business. It begins with the launch of the business, then the growth phase, followed by maturity and decline.

The major takeaway from this infographic is that it takes time to build a business. It takes time for the business to establish itself, generate consistent positive cash flow, and prove their track record.

A major consideration for businesses looking to raise outside capital has to do with the lifecycle stage their business is in. This ties in with the concept of risk vs reward that has played a role so far in determining interest rates for various debt types and the liquidity position of the lender.

The fact is that the majority of business ventures fail. Lenders understand this and perceive risk in the investment to be partially correlated with how long the business has been around. A business that has been around for a decade and can show consistent growth is considered to be a substantially lower risk than a new start up idea that has not generated any cashflow yet.

Although there are some basic business banking products available to start-up businesses, a business without a proven track record will find it nearly impossible to secure any major debt financing in the earliest stages of their business because of this added risk to the investors.

To better understand this principle, see the infographic below, highlighting the risk of lending to or investing in a business based on its lifecycle as well as a business’ ability to get debt funding.

This also explains why start-up businesses often rely on equity investors for outside capital in the beginning.

The perceived risk of default makes debt too risky of an investment because debt repayment is based on cash flow. When debt investors lend a business money, they make their return on that investment from the interest the business pays them on the principle they’ve loaned them. If a business has no consistent positive cash flow, how will the lender reasonably expect them to make monthly or quarterly payments?

Kimberly Advisors is a middle-market investment bank uniquely positioned to help business owners profit through M&A. In addition to M&A transaction brokering, we deliver detailed guidance on growing business value, comprehensive exit planning, and the confidence that comes from partnering with a seasoned M&A advisory team.

%20(1).png)

.png)