This guide explains what term loans are and how businesses use them as a financing option. We also explain the main components of term loans and how they are different from other types of debt. Here are some quick takeaways regarding term loans:

A term loan is an arrangement where a lender gives a business an upfront lump sum of cash for a specific purpose in exchange for the agreed-upon repayment terms of the loan.

Term loans are a type of senior debt. Senior debt is debt where the lender has the highest claim to the borrowing business’ cash flow—meaning that these lenders get paid back before other investors and lenders do.

This guide is part one of a series. After this guide, we recommend: Term Loans (Part 2): Structure & Amortization for a more complete understanding of what term loans are and how they work.

Special Offer For Entrepreneurs

Learn How We Empower Agile Entrepreneurs With The Same Financial Acumen And Strategic Insight As Fortune 500's

Term loans are a type of loan that businesses use to finance specific assets or to finance operational expansion. Term loans give the borrower an upfront lump sum of cash in return for paying the lender back on a schedule, with interest.

Loans consist of several components: the principal, interest, and the term length.

Principal is the face value of the credit the lender is extending to the borrower—it’s the amount of money they’re borrowing. The principal will need to be repaid to the lender by the business (borrower) at some point in the future, as per the agreement.

The amount of money a business can borrow is determined by their creditworthiness, their business lifecycle stage, and their financial strength. Lenders will loan a business up to a multiple of EBITDA and will want to see sufficient interest coverage from the business. We will explain these concepts below.

Interest is the additional charge on top of the principal that’s paid as compensation to the lender in exchange for the risk they take in providing the loan to the business. Here’s an easy way to understand interest from both perspectives: interest is the cost of borrowing the money for the business (borrower), and it’s the compensation that the lender gets in return for loaning the borrower the money.

The interest rate that a business will pay on a term loan is related to both the creditworthiness of the business as well as the market conditions at the time of the loan and with consideration for LIBOR or prime rates at the time of the loan for fixed and for variable interest rate loans.

The term length is the period from when the lender provides the business (borrower) with the cash up until the business has repaid the loan and any interest required, as per the agreement.

The length of the term is usually dependent on the creditworthiness of the business. If the business is perceived to be a higher credit risk, then the term will be less—maybe six months to two years. If the business is seen as low risk from a credit standpoint, then the term may be more like three to five years. Some term loans can be for substantially longer periods of time.

It’s also important to note that term loans can be “stacked” meaning that a business can have multiple term loans at one time—provided by different lenders—that are each structured differently. Each loan will consist of its own principal and interest, it will have its own term length, and these loans will be structured independently and often differently from one another.

We will explain how term loans are structured in the next guide in this series: Term Loans (Part 2): Structure & Amortization. There is more to understanding term loans than is explained here, loans can be amortized or non-amortized, secured or unsecured, and can have variable and fixed interest rates. We recommend finishing this guide before starting that guide, as the next part will build on what is covered here.

Next, we’ll look at what a business uses term loans for.

What Are Term Loans Used For?

Usually, businesses use term loans to finance the purchase of specific assets. Examples of assets term loans are frequently used to purchase include equipment and commercial real estate.

Term loans are for a fixed amount, for a fixed term, and they are associated with a specific purchase or financing endeavor.

In addition to borrowing money to purchase a fixed asset, like real estate, a business can also use term loans to finance operational expansion. However, a business would not generally seek a term loan to borrow excess cash to have on hand in case of an emergency. There are other commercial banking products that are better suited to that end.

In addition to term loans, businesses have access to other banking products and services such as the overdraft on their bank accounts, business credit cards, and revolving lines of credit. Revolving lines of credit and business credit cards are better financing options for dealing with short-term, smaller scale cashflow shortages than term loans are.

Revolving lines of credit differ from term loans in that revolving lines of credit give a business access to a sum of money—up to the maximum amount—and the business only needs to pay interest on the outstanding balance. With revolving lines of credit, unlike term loans, the business doesn’t need to reapply for a new loan each time they need to withdraw money against the balance of the line of credit. To learn more about revolving lines of credit, read this guide.

Term loans are better suited for larger financing endeavors or as a financing arrangement on fixed assets like expensive equipment. It wouldn’t make sense to try and finance these purchases with a revolving line of credit or a credit card.

In this light, term loans can also be used to finance operational expansion, but this would normally only make sense if there was a need for a large upfront lump sum of cash. Otherwise, the business may have better financing options available for smaller purchases or to pay for shorter-term funding gaps.

It’s also worth noting that a business would normally only look to borrow money to finance growth if they are unable to pay for that growth out of cash flow. Financing—whether a term loan or any other banking product or service—comes with fees or interest payments that could be avoided if the business were to grow organically with cash flow from operations.

Now that we understand what term loans are generally used for, we’ll look at the availability of this form of financing at various stages of the business lifecycle.

Term Loans & The Business Life Cycle:

So far, we’ve explained what term loans are, why they’re useful, and we’ve explained how they’re structured. This section will look at the practical reality of getting lenders to give a business a term loan.

The capital stack shows us how a company is financed—it’s a breakdown of a company’s capital structure. The capital stack is generally broken down into three main categories senior debt, subordinated debt, and equity. To learn more about these we recommend our guide: Capital Stack Quick Guide.

Term loans are a type of senior debt.

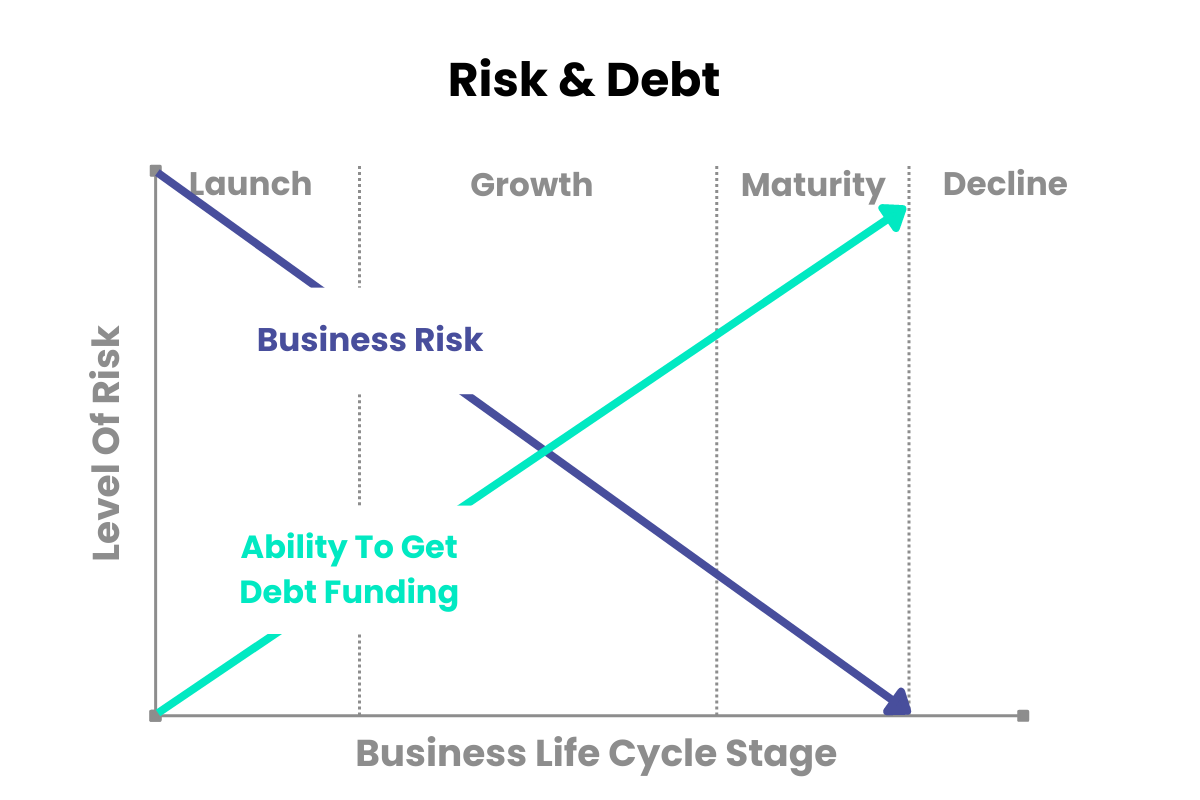

Generally speaking, there is an inverse relationship between time in business and the business’ ability to get debt funding in the form of a term loan. In other words, as a business builds a proven track record with consistent, positive cash flow, lenders perceive it as less of a risk, and that business’ ability to get debt funding becomes more likely.

The business life cycle starts with the launch phase, progresses to the growth phase, followed by maturity and decline. Newer businesses—without a proven track record—are considered a higher risk. This is illustrated below.

This infographic illustrates the perceived risk in lending to a business without a proven track record. It illustrates the inverse relationship between time in business and that company’s ability to get debt funding.

For long-term debt, like a multi-year term loan the lender will want to see financials for the business going back at least three years, but preferably for more than five.

A start-up business without sales wouldn’t be able to show any positive cash flow and they wouldn’t have a proven track record. So, the lender is unlikely to give them a term loan because they have no reason to expect the business to be able to make monthly payments on the loan without cash flow.

This is why start-up businesses often rely on equity financing or are owner-financed in their early stages. Now that we’ve illustrated the perceived business risk based on life cycle stage and the inverse relationship to that business’ ability to get debt funding, let’s look at who provides term loans and what they’re looking for.

Who Provides Term Loans & What Are They Looking For?

Term loans are provided by commercial banks, insurance companies, and credit companies. These companies specialize in these sorts of loans, among other things. Businesses apply for term loans directly with the lender.

Typically, these lenders will be open to providing 2x to 3x a business’ EBITDA. They will also require at a minimum between 1.5x and 2x interest coverage, although an interest coverage ratio above 3 is considered safer. In looking back over these requirements it’s easy to see that lenders are looking for proven track records in the businesses they provide senior debt, such as term loans to.

Lenders providing term loans have the highest claim to the business’ cash flow in the event of default—making term loans less risky than other forms of lending.

Reflecting this lower risk, senior debt generally comes at the lowest cost (interest rate) to the business. While senior debt interest rates can vary widely based on market conditions, the economic climate, and both the creditworthiness of the business as well as its life cycle stage, generally interest rates for senior debt will be 10 percent or less.

Kimberly Advisors is a middle-market investment bank uniquely positioned to help business owners profit through M&A. In addition to M&A transaction brokering, we deliver detailed guidance on growing business value, comprehensive exit planning, and the confidence that comes from partnering with a seasoned M&A advisory team.

%20(1).png)

.png)